Why neutral rates have risen and why it matters

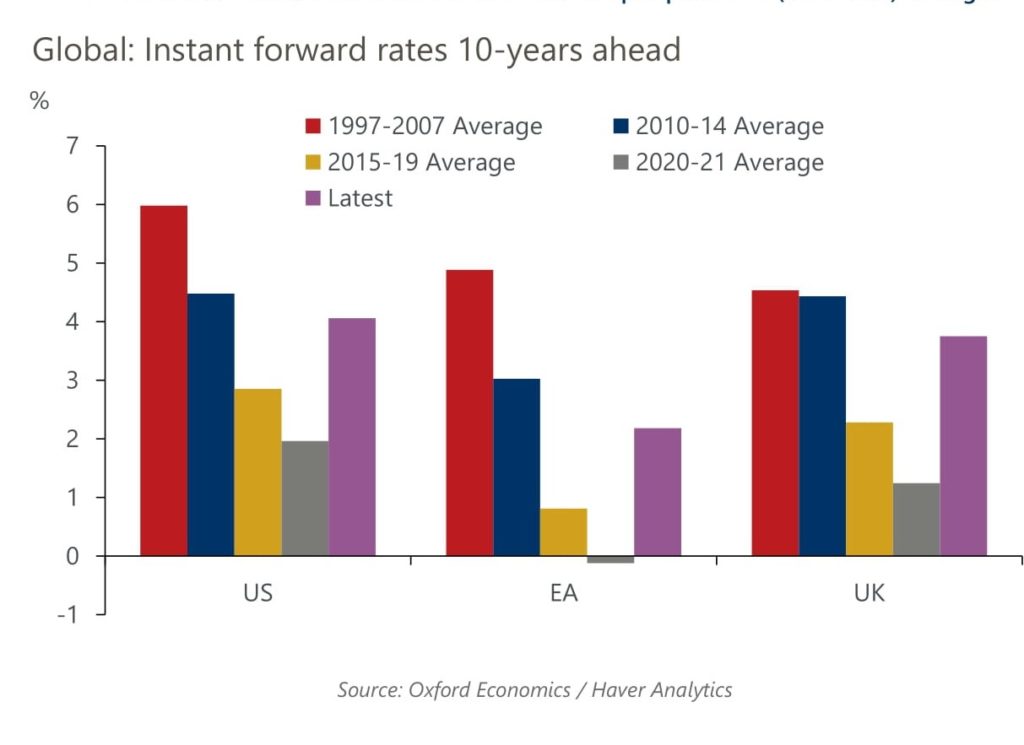

Long-term forward rates have risen markedly in the US, Eurozone, and UK over the last year, and are well above pre-pandemic (2015-2019) averages.

The main driver for this rise in the nominal neutral rates is probably an underlying increase in inflation expectations and consequent increase in nominal pay growth. Meanwhile, the key forces behind the long-term decline in neutral real rates – productivity, demographics, global capital flows – are still in play.

Inflation expectations may remain elevated for some time, reflecting the scarring from the current high inflation rates and an increase in inflation volatility compared to the exceptionally low volatility in the 20 years before the pandemic.

We think it’s likely that the neutral level of nominal interest rates in the coming years will be above the pre-pandemic lows, but still below levels in the pre-global financial crisis period. Uncertainty over both the neutral level of nominal policy rates and the stability of inflation expectations is adding to the challenges facing central banks, making it harder for them to stabilise real activity in line with potential.

Tags:

Related Posts

Post

Japan’s small firms’ profitability will help determine further rate hikes

Rising wage costs have been increasingly squeezing the already low profitability of small firms in Japan, thereby raising concerns about the sustainability of the wage-driven inflation dynamics. The evolution of these dynamics will be key in determining how far the Bank of Japan can raise its policy rate in the coming years

Find Out More

Post

The Economic Impact of Credit Unions

GoWest commissioned Oxford Economics an analysis of credit unions’ economic impact in Arizona, Colorado, Idaho, Oregon, Washington, and Wyoming. The analysis measures credit unions’ economic impacts in terms of GDP, employment, and wages.

Find Out More

Post

US Recession Monitor – Economy entered 2025 on solid footing

A number of recession warnings were flashing yellow and red last year, but the economy didn't falter and entered the year on solid ground.

Find Out More