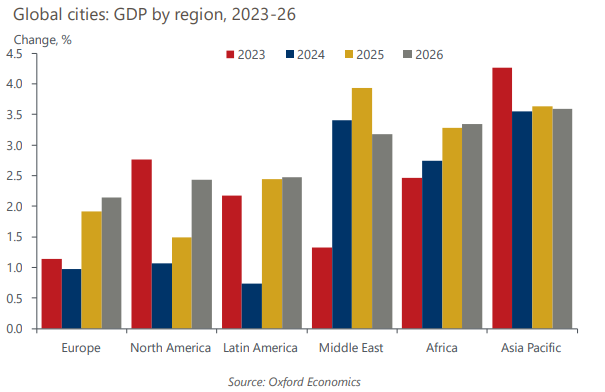

Short-term headwinds to slow GDP growth across major cities

Following a year of subdued global growth in 2023, we think a further softening of economic conditions is likely next year, before activity gathers pace in 2025-26. In this context, we forecast the world’s 1,000 major cities combined will achieve GDP growth of just 2.4% per year over 2024- 26, marking not only a sizeable slowdown from the expected outturn in 2023, but also compared to the 5-year trend of 3.0% per year achieved prior to the pandemic.

What you will learn:

- In 2024, economic growth in many European cities will be hampered by the lagged impact of tighter monetary policies, the recent cost of living squeeze, uncertainty around house prices, and consequent slowdowns in consumer spending. There will, however, be some cities that weather the storm better than others.

- Most North American cities will see GDP growth slow in 2024, with many battling to avoid contractions. Weak activity in interest rate sensitive sectors including finance, insurance, and real estate will be a prominent feature. Latin American cities will also see GDP growth slow sharply in 2024 before rebounding in 2025-26.

- Whilst 2024 will be a challenging year for advanced city economies, many in emerging market cities should see a more positive GDP growth outturn in 2024 than 2023, with those in Africa and the Middle East performing particularly well.

- The short-term outlook for the world’s 20 largest cities is sluggish, especially when compared to pre-pandemic growth. That said, these 20 cities alone will contribute one fifth of the expected GDP increase across the 1,000 cities covered in this analysis.

Tags:

Related Posts

Post

The European housing market has turned a corner, but challenges remain

The housing market across most of Europe has now improved, but has it reached the tipping point?

Find Out More

Post

Calgary, Saint John, and Windsor are the Canadian metros most vulnerable to Trump’s tariffs

Tariff-induced price increases call into question tightly integrated supply chains across North America and make large swathes of exports less competitive.

Find Out More

Post

China coastal tech exporters vulnerable to new Trump tariff

The United States has introduced an additional 10% levy on Chinese imports as part of the opening round of the Trump 2.0 tariff regime. While certainly not as severe as some of the tariff threats made against China by President Trump in the run up to his inauguration, we nevertheless expect the additional tariffs to affect the country’s economic performance—with coastal tech manufacturing hubs particularly vulnerable.

Find Out More