European industry will bottom out and recover…eventually

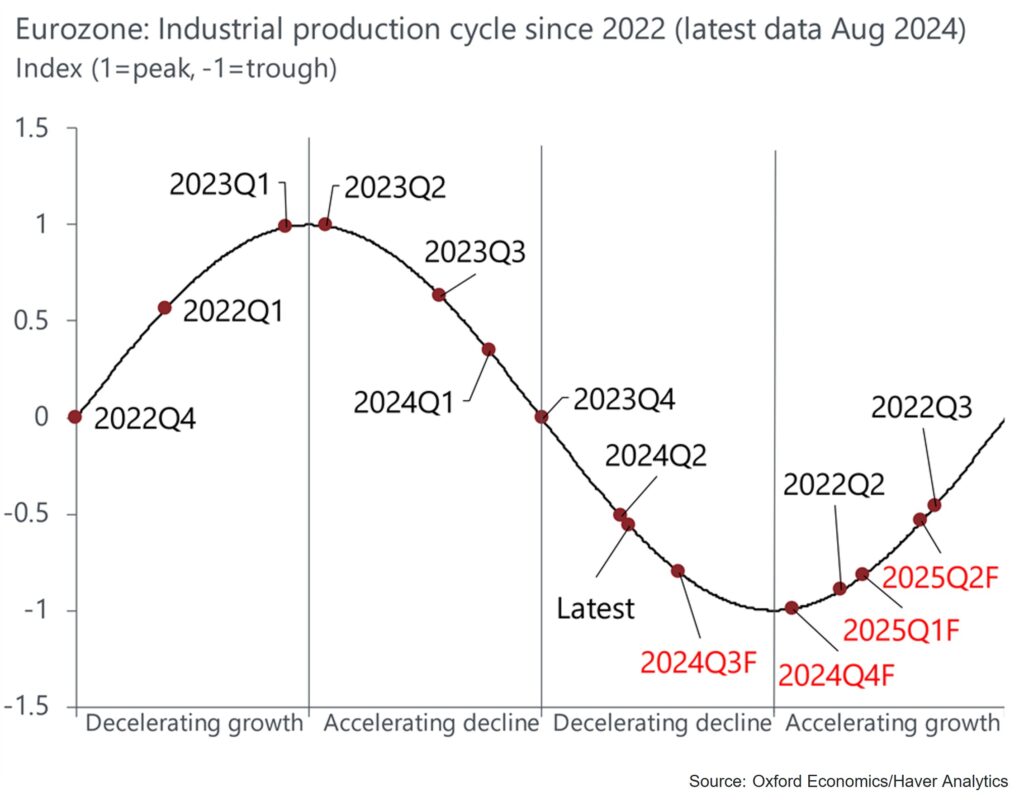

European industry is still in the midst of an almost two-year recession, but we believe that the end is increasingly in sight. Our proprietary business cycle indicator is picking up signs that the pace of decline is moderating which, combined with our forecasts for industrial production, suggests a business cycle trough is approaching.

What you will learn:

- Our latest estimate shows output bottoming out towards the end of this year or beginning of next, setting the stage for an industrial expansion across 2025.

- Falling gas and electricity prices have already provided a boost to energy-intensive sectors, which are at the forefront of growth currently. However, the smaller reach of these sectors means that the broader industrial recovery will have to wait for the effect of interest rate increases to filter through to the real economy, for the inventory cycle to turn, and for consumers’ appetite for goods spending to fully return.

- The risks to our current forecast are firmly on the downside. Weakness in industry has been correlated strongly with weakness in the broader economy, and the eurozone economy has consistently defied expectations it would begin bouncing back.

Tags:

Related Resources

Post

Trump tariff turbulence threatens global industrial landscape

Trump has moved swiftly to advance a trade agenda that goes beyond what was promised in the campaign. This will have a major impact on global industrial prospects.

Find Out More

Post

Europe’s defence splurge will help industry – but by how much?

Our baseline forecast now assumes that European defence spending will rise to 3% of GDP by the end of the decade. This could give a growth boost to Europe's ailing industrial sector.

Find Out More

Post

Blanket tariffs from Trump drag down industrial prospects | Industry Forecast Highlights

The impact of global tariffs, a high degree of policy uncertainty, and higher for longer interest rates are expected to hit industry—we have pushed down our 2025 global industrial production growth forecast by 0.5ppts since our Q4 2024 update.

Find Out More