China sectoral implications of Trump 2.0

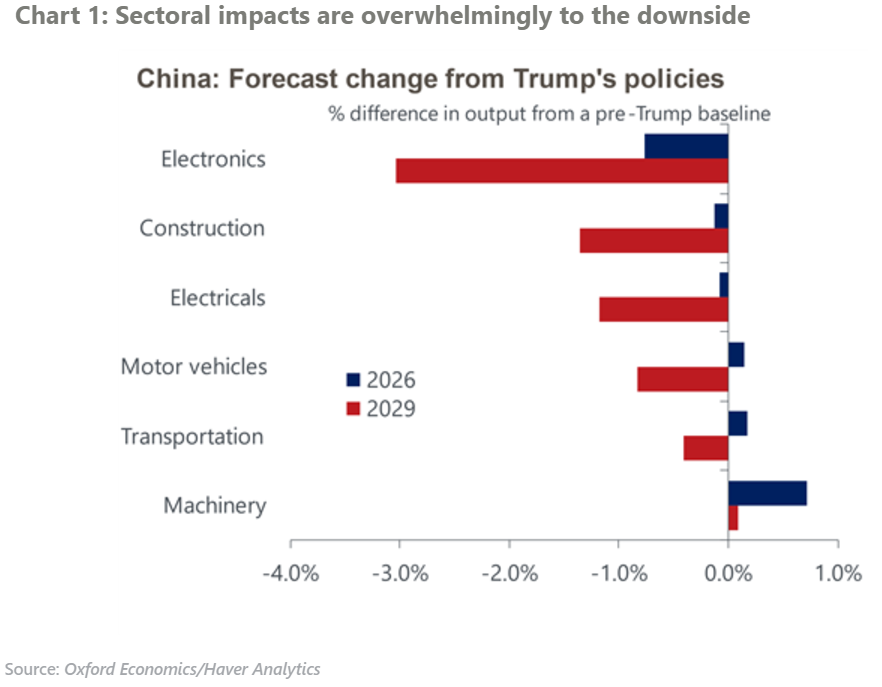

The incoming Trump administration’s trade policies will have significant impacts on China’s sectoral outlook. There will be a small near-term boost to Chinese output prior to the introduction of tariffs owing to a frontloading of orders. However, the long-term impact will be overwhelmingly negative on Chinese industrial activity.

What you will learn:

- Chinese authorities will use fiscal and monetary policy to support the economy, particularly focusing on the property and construction sectors. However, declines in private investment and lower exports to the US will ultimately outweigh the expected fiscal and monetary offsets.

- Supply chains will be disrupted as firms seek to reposition their operations away from China to avoid tariffs. This is particularly true within the automotive and machinery sectors where parts are often traded cross-border multiple times before final assembly. This disruption will be felt most significantly in China, but the impact will be global owing to China’s centrality in global manufacturing.

- The high-tech electronics sector will be amongst the hardest hit. Advanced production will likely migrate to regional peers such as Japan, South Korea, and Taiwan, while lower value-add activities will move towards ASEAN nations. In addition, export restrictions will likely stem the flow of knowledge, hitting productivity and eroding Chinese high-tech competitiveness.

Tags:

Related Posts

Post

Trump tariff turbulence threatens global industrial landscape

Trump has moved swiftly to advance a trade agenda that goes beyond what was promised in the campaign. This will have a major impact on global industrial prospects.

Find Out More

Post

How much could trade policy uncertainty hurt the outlook?

If there’s one thing more damaging than tariffs themselves, it’s the sharp rise in trade policy uncertainty.

Find Out More

Post

No shelter from the external storm for CEE economies

The small, open economies of Central and Eastern Europe (CEE) are struggling against three external headwinds simultaneously: stuttering German industry, protectionist US trade policy, and overcapacity in China's manufacturing sector.

Find Out More