An inflation resurgence remains low on the worry list

The potential resurgence in inflation has led to sharp moves in market interest rate expectations after the Federal Reserve began to cut policy rates. However, we see little evidence that inflation will take a significant turn for the worse, which suggests that the risks of Trump’s policy agenda unleashing sizeable inflationary pressures in the US, and beyond, have been exaggerated.

What you will learn:

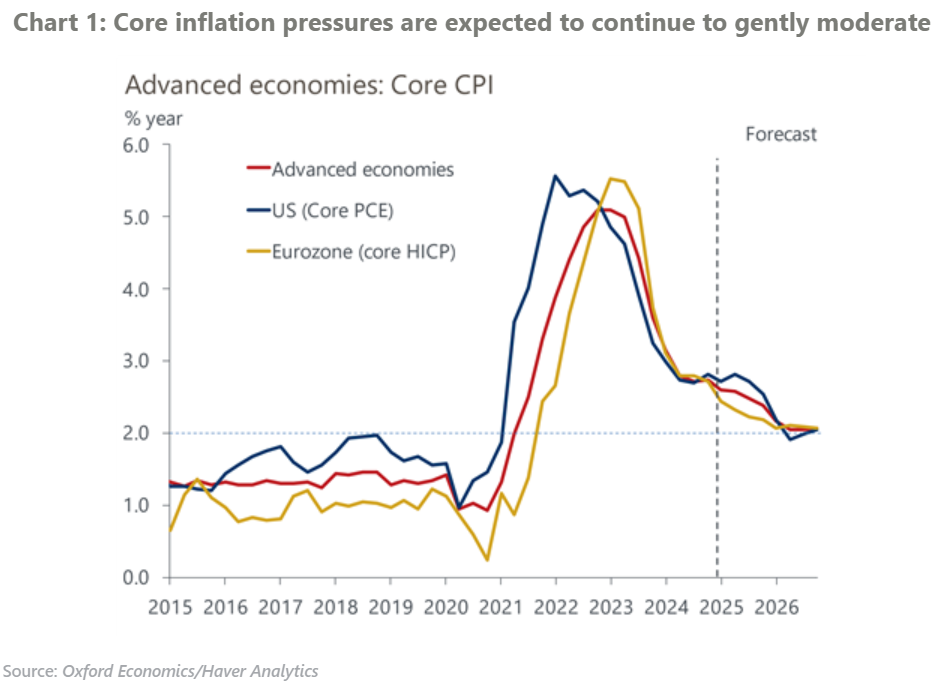

- We’ve long argued that the decline in inflation back to target could prove to be slow and that above-target inflation wouldn’t preclude policy rates from moving into less restrictive territory. Some annual headline inflation measures have recently climbed, but this mainly reflects base effects and shifts in volatile components of the basket, which means there’s no need to panic.

- Future economic policies by the Trump administration could be a catalyst for higher inflation, but our previous work suggests that even a low-probability scenario involving large and broad tariff hikes would have only moderate inflation impacts. Market rate expectations may be placing too much weight on tariffs causing drastic shifts in inflation.

- Although we believe markets overreacted in pricing out future Fed rate cuts beyond this year, we’re even more sceptical that the events of the past month or two warrant an upward readjustment of rate expectations in the Eurozone and the UK. Any evidence of a resurgence in inflationary pressures there is even weaker.

- Aggressive US tariff measures are unlikely to cause highly inflationary retaliatory tariffs. Beyond the shorter term, a significant US tariff shift may likely be more disinflationary than inflationary.

Tags:

Related Services

Post

Japan’s tariff turbulence to flatten near-term growth

We've cut our GDP growth forecasts for Japan by 0.2ppts to 0.8% in 2025 and by 0.4ppts to 0.2% in 2026, reflecting higher US tariffs and heightened global trade policy uncertainty. We now forecast that Japan's economy will barely grow over 2025-2026 on a sequential basis.

Find Out More

Post

Growth outlook cut further for the Eurozone amid tariff turmoil

Given the unique nature of the hike in US tariffs, the size of these supply and demand shocks and the speed at which they are arriving make the precise economic implications particularly hard to pin down. Overall, however, we expect GDP growth in the US and world economy to slow sharply, but we don't anticipate recessions in either.

Find Out More

Post

Inflation is on the rise in Saudi Arabia, should we be worried?

Saudi Arabia’s inflation rose to 2.3% in March, its highest level since July 2023, driven mainly by a faster rise in food and beverage prices.

Find Out More