An inflation resurgence remains low on the worry list

The potential resurgence in inflation has led to sharp moves in market interest rate expectations after the Federal Reserve began to cut policy rates. However, we see little evidence that inflation will take a significant turn for the worse, which suggests that the risks of Trump’s policy agenda unleashing sizeable inflationary pressures in the US, and beyond, have been exaggerated.

What you will learn:

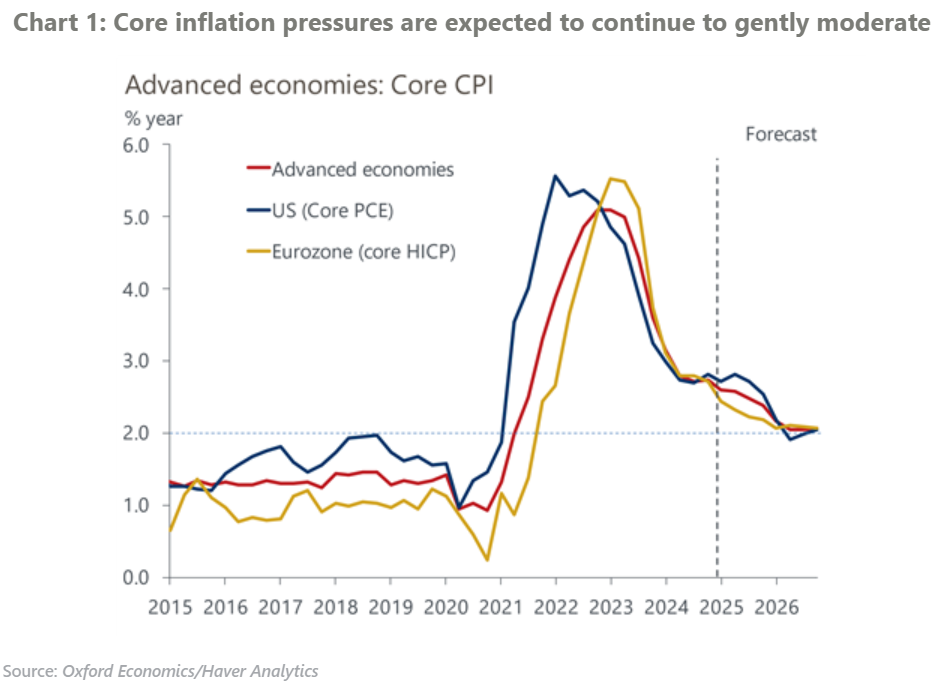

- We’ve long argued that the decline in inflation back to target could prove to be slow and that above-target inflation wouldn’t preclude policy rates from moving into less restrictive territory. Some annual headline inflation measures have recently climbed, but this mainly reflects base effects and shifts in volatile components of the basket, which means there’s no need to panic.

- Future economic policies by the Trump administration could be a catalyst for higher inflation, but our previous work suggests that even a low-probability scenario involving large and broad tariff hikes would have only moderate inflation impacts. Market rate expectations may be placing too much weight on tariffs causing drastic shifts in inflation.

- Although we believe markets overreacted in pricing out future Fed rate cuts beyond this year, we’re even more sceptical that the events of the past month or two warrant an upward readjustment of rate expectations in the Eurozone and the UK. Any evidence of a resurgence in inflationary pressures there is even weaker.

- Aggressive US tariff measures are unlikely to cause highly inflationary retaliatory tariffs. Beyond the shorter term, a significant US tariff shift may likely be more disinflationary than inflationary.

Tags:

Related Services

Post

Weaker core inflation makes a February rate cut a possibility in Australia

CPI inflation was weak once again in Q4, with the headline measure increasing by just 0.2% q/q. Inflation has now slowed to 2.4% y/y. The trimmed-mean measure increased by 0.5% q/q in Q4, which is an encouraging step down.

Find Out More

Post

The RBA faces mixed signals ahead of the February meeting in Australia

We've lowered our 2025 GDP growth forecast for Australia by 0.1ppt to 1.9% due to a weaker outlook for near-term population growth.

Find Out More

Post

Eurozone: Euro will cushion, but not offset, the tariff impact

Despite the recent appreciation, our forecast still sees a weaker euro versus the US dollar compared to our pre-US election baseline. We think this will partially mitigate the adverse growth impact of tariffs. But extra-Eurozone exports have become less sensitive to a weaker euro over time, so currency depreciation cannot be relied on to offset the adverse impact of price shocks on Eurozone exports.

Find Out More