Japan expects mixed impacts from Trump’s second presidency

We’ve adopted our “limited Trump scenario” as our baseline forecast for Japan. We now assume that the US will impose targeted tariffs on Japan’s exports, among several other economies. We think these measures will have a limited impact on overall growth, but globally higher trade barriers are likely to hit Japanese manufacturers’ profitability and financial markets. In addition, there is a non-negligible risk that Trump could implement even stricter tariffs.

What you will learn:

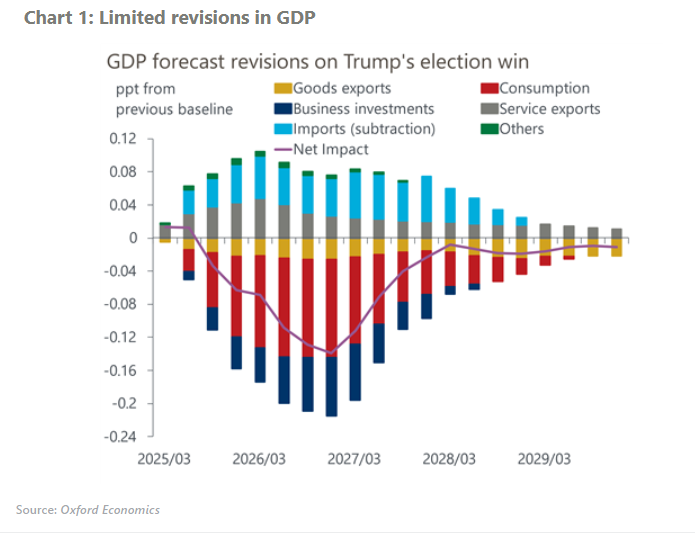

- Given Japan’s sizeable trade surplus against the US, we assume that the US will impose 10% tariffs on Japanese autos and base metals from 2026. The direct impact from additional tariffs on Japan’s exports will be limited. That said, we are revising down our export outlook for Japan given weaker capital goods demands ahead, though it will be partially offset by a stronger US economy supported by looser fiscal policy.

- In addition, we are downgrading our near-term projections for domestic demand. Businesses are likely to hold back capex activities amid high economic policy uncertainty. We think that policy uncertainty in the US matters as much as domestic policy for business investment decisions in Japan. Weaker household real income gains will limit consumption.

- Under our less likely “global trade war” scenario, the economy would suffer from higher tariffs, weaker global demand, and further yen depreciation. Also, recently announced 25% tariffs on Canada and Mexico, if realised, could hit the auto sector as they have invested heavily in Mexico.

For more insights on the 2024 US Presidential Election, click here.

Tags:

Related Posts

Post

Japan’s politics add uncertainty to BoJ policy outlook

The Bank of Japan (BoJ) kept its policy rate at 0.5% at its October meeting, after a 7-2 majority vote. Two board members again voted for a rate increase. We believe the BoJ will hike in December to 0.75% as incoming data confirm that the economy is performing in line with the bank's forecasts in its quarterly outlook. However, there's a material chance of a delay.

Find Out More

Post

Japan’s December rate hike appears likely, though there is a risk of delay

We've brought forward the timing of the next Bank of Japan (BoJ) 25bps rate hike to December from next year and have added another 25bps hike in mid-2026. This reflects the surprisingly hawkish shift in the BoJ's view since its September policy meeting and upward revisions to our growth and inflation projections, driven by the US economy's resilience.

Find Out More

Post

BoJ announces cautious plan to sell ETF and J-REIT holdings

At its monetary policy meeting on Friday, the Bank of Japan (BoJ) unexpectedly announced it would start to sell its ETF and Japanese real estate investment trust (J-REIT) holdings. We think the impact of this plan on financial markets will likely be limited because the BoJ is opting to play it safe in terms of the process and the scale.

Find Out More